21

Apr 2026

Hormuz Shock → Africa Real Assets: Why a Middle East War Becomes an African DSCR Event

By Sir Felix Modebe B.Sc., M.Sc., MBA, FRICS, CCIM, KSJI

Visionary Founder-Leader | N3 CAPITAL AFRICA

The Strait of Hormuz is often discussed as geopolitics. For allocators underwriting African real assets as infrastructure-grade exposures, Hormuz is better framed as a cashflow pipeline. The shock is not the headline; it is the mechanism by which input costs, FX friction, logistics premiums and refinancing repricing migrate into African asset waterfalls.

The current conflict—sparked by joint U.S.-Israeli strikes on Iran on February 28, 2026—has evolved into an energy-and-shipping disruption centered on Hormuz. The structural point is straightforward: when a chokepoint concentrates global crude and LNG flows, price and availability risk propagates rapidly into import-dependent systems, and then into DSCR.

The load-bearing data is not abstract. EIA estimates that flows through Hormuz in 2024 and early 2025 represented more than one-quarter of global seaborne oil trade and about one-fifth of global oil and petroleum product consumption. EIA separately notes that in 2024 roughly 20% of global LNG trade transited Hormuz, largely Qatar-linked. The IEA similarly highlights the scale of LNG transit through the strait.

If the pipeline is disrupted, the underwriting question is not “what is Brent doing?” It is: where does the shock land inside the cashflow hierarchy—and which covenants trigger first?

Structural diagnosis: why conventional approaches fail

Conventional structuring in African real assets often fails during global shocks for one recurring reason: enforcement sits outside the waterfall.

- The contract exists (PPA, concession, lease), but collections are not ring-fenced.

- The asset is “USD-linked,” but FX convertibility and transferability are treated as macro assumptions, not as timing risks with engineered cures.

- OPEX volatility—particularly diesel and logistics—is modelled, but not capitalised into reserves and not connected to distribution gating.

- Refinancing is assumed to be available because “the asset is strategic,” even when the structure contains maturity cliffs and thin coverage cushions.

In a Hormuz-type shock, those weaknesses convert directly into DSCR compression, arrears accumulation and delayed cures—long before the asset is in a legal default.

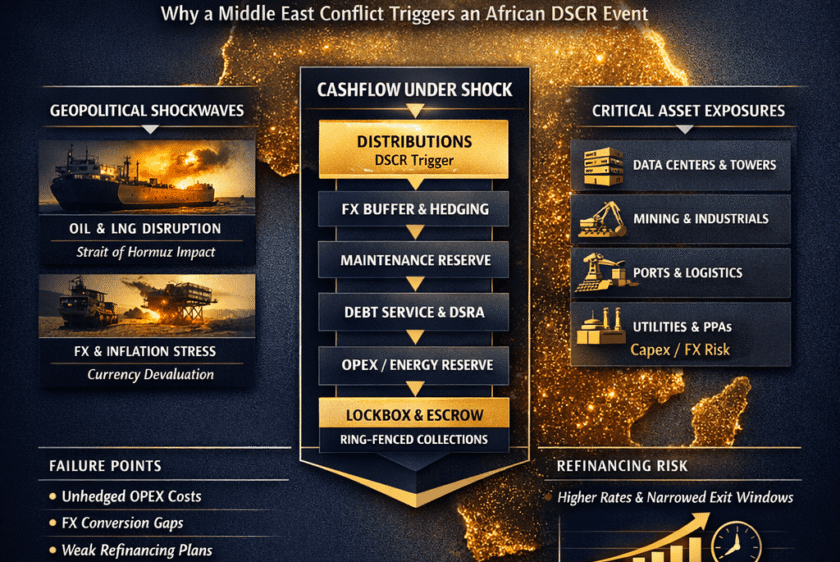

Engineering framework: the 4 shock rails, translated into structure

N3’s structural lens treats the current episode as four shock rails that must be converted into controls.

Rail 1: Energy rail — diesel + grid gaps = OPEX shock (DSCR compression)

Across multiple African markets, the marginal kWh for critical assets still becomes “diesel-backed” under grid instability. The transmission is immediate: higher fuel prices → higher unit energy cost → EBITDA compression → lower DSCR. This is most acute for data centres, towers, cold-chain logistics, industrial power users, hospitals and malls, and for mining where diesel is a major variable cost.

The question for allocators is whether diesel exposure is merely “an operating line,” or whether it is treated as a structural risk with ranked reserves and triggers. In a shock, the asset does not fail because it lacks revenue; it fails because OPEX volatility enters the waterfall before discipline does.

Rail 2: FX rail — imported inflation → tighter policy → weaker local currency

Energy inflation transmits into CPI, fiscal stress and policy tightening. We are already observing state responses that are explicitly inflation- and fuel-driven. Kenya has sought rapid World Bank support, cut fuel VAT temporarily, revised growth down, and cited reserves above $13bn (~5.8 months of imports) while pausing rate cuts. Nigeria has flagged the war as worsening inflation pressures; Reuters reported petrol prices up >50% and diesel up >70% in this context.

In structures that claim “USD-linkage,” the real risk is frequently conversion timing and transfer approvals, not headline FX levels. If conversion is delayed, the waterfall must respond automatically.

Rail 3: Logistics rail — freight/insurance premiums → capex creep & delays

Even domestic assets import critical components: solar modules and inverters; turbines and spares; IT and cooling equipment; replacement parts for gensets. During conflict-driven shipping stress, capex rises and schedules slip. This is not a project-management detail; it is a refinancing risk. Delays extend construction interest, weaken covenant headroom, and can convert a bankable asset into a take-out problem.

Rail 4: Capital markets rail — risk-free up, spreads wider, take-out windows narrow

Conflict-linked energy shocks raise inflation pressures and can keep monetary conditions tighter. The New York Fed’s John Williams explicitly flagged war-driven inflation pressures via energy pass-through. Mechanically, higher risk-free rates and wider spreads reprice take-out windows and shorten tenors unless structures are hardened.

The same shock can also disrupt product markets; the IEA has discussed impacts on refined products and constraints when flows through Hormuz are impaired. The institutional takeaway remains: refinancing visibility is not a forecast; it is an engineered outcome.

“KPI → Trigger → Remedy”: converting rails into enforceable controls

For insurance balance sheets and DFI co-investors, the discipline is to convert each rail into a measurable KPI that triggers a remedy inside the structure.

Example control set (illustrative):

- KPI: Net energy cost / unit (or diesel cost per kWh) increases beyond a preset band

- Trigger: sustained breach over 30–60 days

- Remedy: automatic top-up of Fuel/Energy Reserve before distributions; step-up in minimum DSCR for distributions; temporary distribution lock

- KPI: DSCR (and forward-looking DSCR) falls below threshold

- Trigger: DSCR < 1.20x (example) or forecast DSCR breach within next quarter

- Remedy: cash trap, accelerated amortisation, mandatory OPEX efficiency plan under independent oversight

- KPI: FX conversion / transfer delay days exceed covenant limit

- Trigger: delay > X days (country-specific, contract-specific)

- Remedy: FX delay trap: all surplus cash retained; cure plan; draw on FX buffer/DSRA permitted under rules; sponsor support or reserve replenishment required prior to distributions

- KPI: Construction schedule variance or capex overrun exceeds threshold

- Trigger: delay > X days or capex +Y%

- Remedy: sponsor equity top-up; contingency reserve top-up; revised completion tests; substitution rights for EPC under defined failure conditions

This is the difference between “robust documentation” and a structure that can be allocated to in a tightening regime.

Stress-case analysis: what resilience looks like under four scenarios

A credibility-stage insight must show how the structure behaves under stress, not merely why the risk exists.

Scenario A: FX shock + conversion delays

Resilient structures treat FX as a timing problem. Lockbox, ranked reserves and FX delay traps preserve senior debt service even when transfers are slow, while preventing structural leakage to equity.

Scenario B: Fuel-driven OPEX shock (diesel pass-through absent)

Resilience requires either: (i) contractual pass-through, or (ii) pre-funded reserves and distribution gating. Without those, DSCR becomes volatile and covenant breaches become frequent, pushing assets into renegotiation cycles.

Scenario C: Revenue disruption / payment delays (offtaker stress)

Resilience is the presence of arrears mechanics inside the waterfall: cure periods, step-in rights, escrow discipline, and replacement O&M provisions that can execute.

Scenario D: Refinancing repricing

Resilience is amortisation sculpting and visible take-out engineering: maturity ladders, conservative leverage, and refinance triggers that start early—before the market closes.

Institutional implications: what clears IC thresholds now

For insurance allocators, the clearances are not rhetorical. They are structural:

- Cashflow integrity: ring-fenced collections, ranked reserves, distribution gating

- Governance enforceability: step-in rights, substitution clause, independent oversight, AssetCo/HoldCo control

- Duration alignment: amortisation sculpting, DSCR buffers, maturity discipline

- Exit visibility: documented take-out pathways, covenant-based early warning, and cure mechanics that do not depend on goodwill

Africa will continue to experience global shock transmission. The allocability question is whether each platform is engineered to contain risk migration and preserve covenant resilience.

Controlled strategic close

If Hormuz teaches that energy shocks immediately become FX and DSCR events, the next underwriting question is more uncomfortable: when global liquidity tightens and take-out markets ration tenor, what protects refinancing visibility in jurisdictions where enforcement timelines are uneven—and which governance controls actually survive cross-border stress?