01

Apr 2026

Security Perfection in Practice: Title, Consents, and Enforceability Timelines

By Sir Felix Modebe B.Sc., M.Sc., MBA, FRICS, CCIM, KSJI

Visionary Founder-Leader | N3 CAPITAL AFRICA

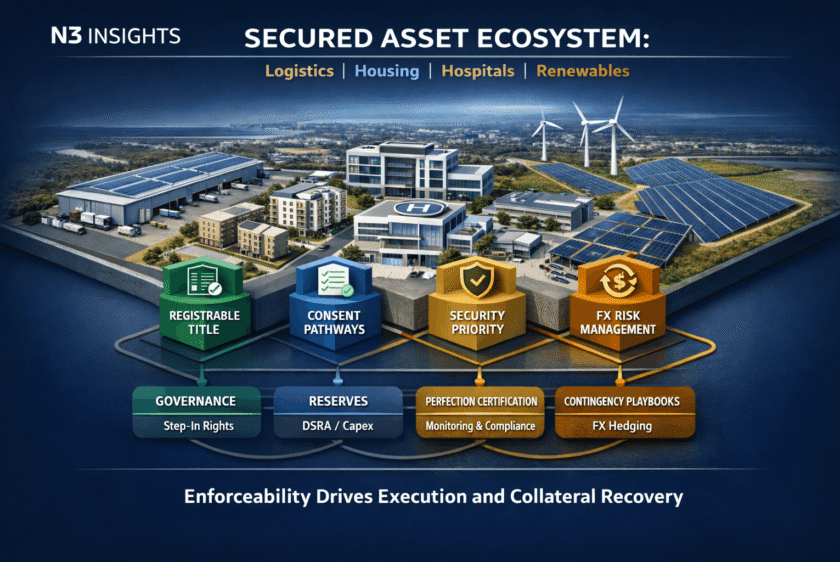

Enforceability Is the Underwrite

Across logistics/industrial, housing, hospitals, and renewables, the constraint is not demand. It is enforceability. Cash controls, FX risk, utilities uptime, and exitability all depend on whether title is registrable, security is perfected, and remedies are practical within an investable timeline. In many frontier markets, value is lost not at entry but during enforcement friction—consent gaps, priority disputes, permit lapses, or utility interruptions that impair cash sweeps. The underwriting consequence is clear: perfection planning and dispute sequencing must be embedded at term sheet, not retrofitted at default.

What Changed: From Asset Buying to Platform Underwriting

Underwriting has shifted from document sufficiency to execution sufficiency. Investors now diligence registrability, priority ranking, and consent pathways alongside cash flow. Documentation increasingly embeds reporting triggers tied to perfection steps, not only performance. Governance rights are calibrated to enforceability risk, with conditional step-in rights and pre-agreed cure periods. Exit readiness is assessed through transferability of security and consent portability.

Asset buying prices a building. Platform underwriting prices the ability to replicate title, consents, and enforcement across sites without resetting risk.

Sector Controls: What Pays, What Breaks, What Fixes

Logistics / Industrial.

Investors pay for long-tenor leases, credit tenants, indexation, and uptime. Bankability breaks on defective title, unregistered long leases, utility dependence without redundancy, or concentration risk. Risk owner: sponsor for title and permits; tenant for lease compliance; operator for uptime. Enforceability: registered mortgages/long leases; fixed and floating charges; direct agreements with utilities and tenants. Monitoring: perfection certificates prior to first draw; quarterly title status reporting; utility outage triggers linked to cash sweeps and capex reserves.

Housing (rental platforms).

Investors pay for occupancy durability and indexed rent flows. Bankability breaks on fragmented title, consent-to-assign constraints, or informal tenancies. Risk owner: sponsor for aggregation and clean title; manager for tenancy compliance. Enforceability: portfolio-level security with site schedules; escrowed rent accounts; enforceable property management agreements. Monitoring: monthly occupancy and arrears triggers; covenant lock-ups where arrears exceed agreed thresholds; lifecycle reserve adequacy reviews.

Hospitals (availability or hybrid revenue).

Investors pay for counterparty quality and clinical uptime. Bankability breaks on land-use misalignment, environmental consents, or step-in resistance from operators. Risk owner: sponsor for land and permits; operator for service delivery; offtaker for payment discipline. Enforceability: perfected land mortgage; assignment of receivables; direct agreements granting step-in rights; reserve accounts for O&M and insurance. Monitoring: service-level reporting; payment delay triggers; governance rights to replace operator upon persistent breach.

Renewables (land-intensive).

Investors pay for contracted offtake, grid access, and indexation. Bankability breaks on land tenure disputes, incomplete grid consents, or convertibility friction. Risk owner: sponsor for land and grid permits; offtaker for payment; government for convertibility undertakings. Enforceability: registered land rights; security over project accounts; offtake assignment; FX ring-fencing where feasible. Monitoring: construction milestone certifications; grid-connection condition precedent; FX liquidity triggers activating contingency playbooks.

Country Lens: Priority Markets and Watchlist

Nigeria. FX pathway depends on documented inflow registration and banking channels. Title requires governor’s consent; timing affects priority. Permits can be sequential; utilities reliability varies by corridor. Enforcement is viable but time-bound; monitoring must track consent issuance and registry stamping before full disbursement.

South Africa. Mature registries and priority clarity support bankability. FX is generally workable within regulatory parameters. Permits are structured; utilities reliability is a known operational risk. Enforcement is practical; lenders should monitor covenant compliance and utility backup sufficiency.

Kenya. Title registration is established but due diligence must address historical encumbrances. FX convertibility depends on banking processes. Permitting is defined yet subject to sequencing. Enforcement is feasible; reporting triggers should track land registry updates and environmental approvals.

Ghana. Land title reforms improved clarity, though consent pathways can extend timelines. FX access depends on documentation discipline. Utilities reliability varies. Enforcement is workable; condition precedents should include final land certificates and utility agreements.

Côte d’Ivoire. OHADA framework supports security structures; registrability is central. FX is linked to regional monetary arrangements. Permits are structured; utilities reliability depends on zone. Enforcement benefits from commercial court processes; monitoring should focus on registry confirmation and contract enforceability.

Watchlist.

Tanzania: land tenure categories require precise structuring; FX monitoring essential.

Namibia: strong registry integrity; utilities generally stable; enforcement practical.

Zambia: FX convertibility risk requires ring-fencing and contingency reserves.

Rwanda: streamlined permits; smaller market depth; enforcement generally efficient.

Control Stack: Enforceability Checklist

- Governance. Board observer rights; reserved matters on land transfer; conditional step-in rights; independent security trustee.

- Financial covenants. Illustrative DSCR/LLCR floors; cash sweeps; distribution lock-ups; equity cure rights with limits; concentration caps.

- Reserves. DSRA; lifecycle and O&M reserves; insurance proceeds waterfall; capex pre-funding where utilities are fragile.

- Reporting triggers. Perfection certificates prior to draw; quarterly registry confirmations; permit renewal calendar; arrears and uptime dashboards.

- FX mitigants. Ring-fenced project accounts; documented inflow registration; gated distributions; contingency playbooks for convertibility delays.

Each control assigns ownership, defines a remedy path, and sets a monitoring cadence. Without that triad, security is theoretical.

Board Implications

First, tenor must match enforceability timelines, not just asset life.

Second, pricing discipline should reflect consent and registry risk, not only cash yield.

Third, replication logic requires standardized perfection protocols across sites.

Fourth, governance must be calibrated to step-in practicality, not symbolic rights.

Fifth, “institutional-ready” means registrable, enforceable, and monitorable.

At N3 CAPITAL AFRICA, we treat perfection planning as a core underwriting workstream.

For allocators: are your investment committees underwriting cash flow, or are they underwriting the certainty of enforcing it when it matters?