16

Mar 2026

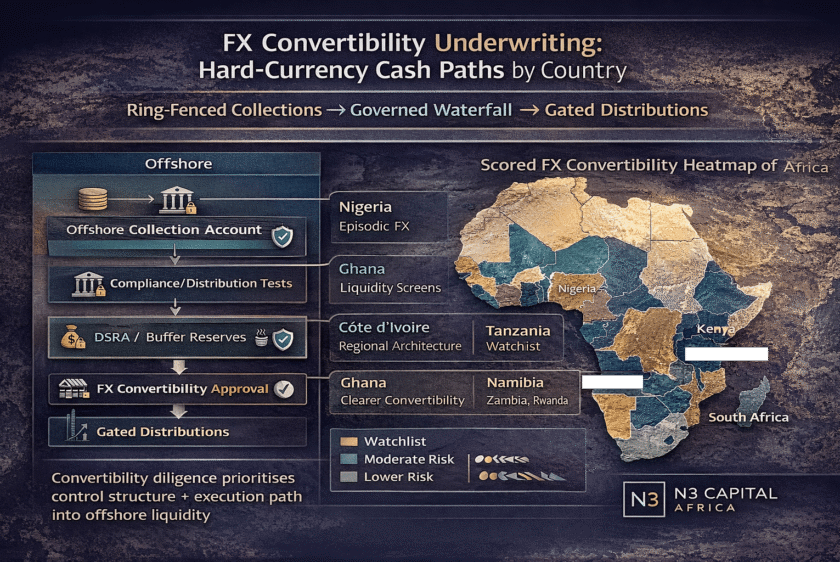

FX Convertibility Underwriting: Hard-Currency Cash Paths by Country

By Sir Felix Modebe B.Sc., M.Sc., MBA, FRICS, CCIM, KSJI

Visionary Founder-Leader | N3 CAPITAL AFRICA

FX convertibility is no longer a macro footnote in African real assets. It is a core driver of bankability because it determines whether contracted local cash can become serviceable hard-currency liquidity on schedule. The underwriting consequence is practical: committees fund assets where cash movement is engineered as a control system—ring-fenced collections → governed waterfall → gated distributions—with documented remedies when convertibility tightens. This shifts diligence from “FX views” to cash-path executability, enforcement practicality, and monitoring cadence.

What Has Changed in Institutional Standards

Institutional standards have tightened around three requirements: (i) cash must be controllable, (ii) convertibility stress must have pre-agreed mitigants, and (iii) governance must remain executable in downside. Documentation now specifies offshore/onshore account architecture, distribution tests, cure mechanics, and dispute paths. Reporting cadence is moving to monthly cash movement packs and quarterly certifications that link triggers to remedies. This is the difference between “asset buying” and “platform underwriting”: the latter requires a repeatable cash-control spine that performs across jurisdictions, not a one-off structuring memo.

Where Capital Is Allocating and Why

Digital infrastructure (data centres, towers, fibre)

- Investors pay for: contracted revenues, uptime discipline, credible EnergyCo layer, hard-currency payer pathways where feasible.

- Breaks bankability: convertibility delays, utility fragility, counterparty concentration, SLA disputes.

- Controls: offshore collection accounts, distribution gating tied to cash-movement triggers, uptime KPIs with cure-to-terminate ladder, step-in rights, and incident reporting triggers.

Healthcare platforms

- Investors pay for: diversified revenue, governed payer mix, predictable collections conversion, utilities uptime as a continuity layer.

- Breaks bankability: arrears and working-capital stress, FX-driven consumables inflation, downtime events, operator dependency.

- Controls: lockbox + waterfall discipline, AR aging triggers with cure periods, pass-through rules where feasible, reserve accounts for O&M/lifecycle, and governance rights to replace underperforming operators.

Logistics platforms

- Investors pay for: lease durability, tenant quality, export-linked demand, logistics uptime, inflation-linked terms.

- Breaks bankability: title/security gaps, capex backlog, tenant concentration, FX mismatch where costs are imported.

- Controls: concentration caps, capex gates, controlled collections, distribution tests linked to DSCR/LLCR (illustrative thresholds), and reporting on occupancy, arrears, and maintenance backlog.

Renewables with contracted offtake (grid-adjacent)

- Investors pay for: contracted offtake, enforceable payment mechanics, operational availability, E&S discipline.

- Breaks bankability: payment delays, curtailment, convertibility bottlenecks, change-in-law exposure.

- Controls: ring-fenced revenue accounts, DSRA where levered, availability KPIs with remedies, defined dispute path timelines, and distribution gating during convertibility stress.

Country Signals for Bankability

Nigeria: FX pathway can be episodic; title/security is diligence-heavy; permits vary by state; utilities reliability often requires captive solutions; enforcement improves with tight security perfection and a practical dispute path. Structuring implication: prioritize ring-fencing, waterfall discipline, and distribution gating tied to cash-movement triggers.

South Africa: Convertibility is generally clearer; title/security systems are robust; permitting is process-driven; grid constraints elevate uptime/back-up requirements; enforcement is comparatively predictable. Implication: focus on performance covenants and resilience capex governance more than convertibility workarounds.

Kenya: FX management is central; title/security is workable with rigorous process; permitting can be time-variable; utility reliability differs by corridor; enforcement benefits from explicit cure mechanics and direct agreements. Implication: design gated distributions and evidence-led reporting that tracks convertibility and utility continuity.

Ghana: FX and liquidity management remain relevant; title/security requires verification; permits are sequential; utilities performance still underwritten; enforcement improves with clear remedies and monitoring cadence. Implication: define convertibility stress triggers and pre-agreed cash buffers with accountable owners.

Côte d’Ivoire: FX pathway can benefit from regional architecture; title/security and permits are improving with process; utilities reliability varies by zone; enforcement practicality rises with standardized security and reporting. Implication: build a repeatable cash-path template and covenant reporting suitable for refinance.

Tanzania (watchlist): Convertibility can tighten; title/security requires disciplined execution; permits are sector-dependent; utilities reliability necessitates redundancy standards; enforcement is strongest with practical remedy timelines.

Namibia (watchlist): FX convertibility is generally clearer; title/security confidence is stronger; permitting is orderly; power constraints require contingency; enforcement is practical when security is properly perfected.

Zambia (watchlist): FX volatility is a primary risk; title/security diligence is critical; permits can be timing-sensitive; utilities reliability varies; enforcement improves with staged remedies and direct agreements.

Rwanda (watchlist): FX management is disciplined; title/security processes are structured; permitting is more predictable; utilities still require uptime covenants; enforcement benefits from clear governance escalation.

IC Control Stack: Minimum Requirements

- Governance: reserved matters; related-party controls; capex approvals; operator replaceability; escalation ladder with accountable owners.

- Financial covenants: DSCR/LLCR (illustrative floors); distribution lock-up; cash sweeps; cure periods with remedy timelines.

- Reserve accounts: DSRA where levered; lifecycle capex; O&M/spares/insurance reserves with replenishment rules and draw governance.

- Reporting triggers: monthly cash-movement pack; quarterly covenant certificate; annual audit; incident escalation playbooks (time-bound).

- FX mitigants: ring-fenced accounts; offshore collection where feasible; distribution gating tied to convertibility delay triggers; pre-agreed contingency playbooks (who acts, by when, with what remedy).

N3 CAPITAL AFRICA’s operating view is that convertibility risk is best treated as a governed workflow, not a forecast.

Board Decisions and Open Questions

Boards should decide, explicitly:

- The minimum cash-path architecture required before underwriting tenor.

- The governance rights needed to enforce remedies across borders.

- The reporting standard that qualifies an asset as institutional-ready.

- The replication rulebook that prevents bespoke exceptions from scaling risk.

- The conditions under which distributions are gated versus accelerated.

Serious allocator question: what convertibility evidence and enforceable cash controls should be non-negotiable before approving long-tenor exposure in each of these markets—regardless of sector?