07

Apr 2026

Pan-African Infrastructure as Institutional Asset Class: From Narrative to Cashflow Hierarchy

By Sir Felix Modebe B.Sc., M.Sc., MBA, FRICS, CCIM, KSJI

Visionary Founder-Leader | N3 CAPITAL AFRICA

1. Institutional Framing: Allocability Begins with Cashflow Hierarchy

Pan-African infrastructure is frequently discussed as a development theme. Institutional capital does not allocate to themes. It allocates to exposures capable of preserving cashflow integrity across cycles, jurisdictions and political regimes.

The institutional question is not whether infrastructure demand exists. The structural question is whether revenue enforceability, covenant resilience and duration alignment are engineered before capital is introduced.

An infrastructure platform becomes an asset class only when its cashflow hierarchy is predictable, enforceable and insulated from discretionary interference. Without that hierarchy, it remains a project. With it, it becomes allocable capital stock.

For sovereign wealth funds operating under intergenerational mandates, allocability is not optional discipline — it is fiduciary requirement.

2. Structural Diagnosis: Why Conventional Infrastructure Framing Fails

Conventional infrastructure narratives rely on macro demand, urbanisation statistics or GDP growth correlation. These inputs are economically relevant but institutionally insufficient.

Three structural misalignments consistently undermine allocability:

First, revenue without enforceability.

Tariffs exposed to renegotiation, volume-based projections without sovereign support, and discretionary payment flows create structural leakage.

Second, duration mismatch.

Concession tenors misaligned with amortisation sculpting create refinancing risk before asset maturity stabilises.

Third, governance opacity.

Absence of escrow discipline, distribution gating and covenant triggers allows equity extraction before downside containment is secured.

In each case, the deficiency is not opportunity scarcity. It is structural under-engineering.

Institutional allocators do not reject African infrastructure because of geography. They reject weak cashflow hierarchy.

3. Engineering Framework: Converting Infrastructure into Institutional Exposure

I. Revenue Enforceability Architecture

Institutional infrastructure relies on revenue frameworks where risk migration is deliberate.

Availability-based contracts, indexed leases and hard-currency PPAs shift demand volatility away from the platform and toward contracted counterparties with defined payment obligations.

Revenue must be:

- Contracted

- Indexed or USD-linked

- Ring-fenced through escrow discipline

- Backed by termination compensation regimes

Without these elements, projected yield remains theoretical.

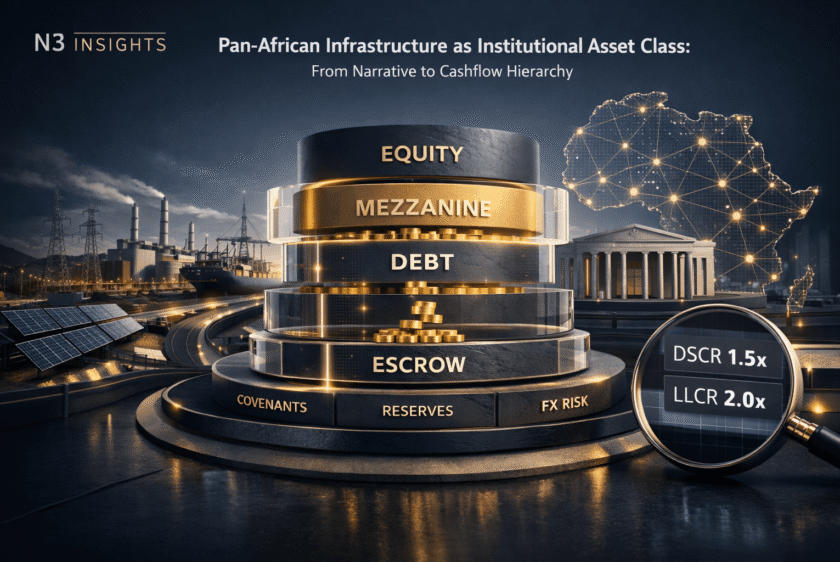

II. Escrow Discipline and Waterfall Sequencing

Cashflow hierarchy begins at collection.

All revenues should flow through controlled escrow accounts with waterfall sequencing prioritising:

- Senior secured debt

- Reserve buffers

- Mezzanine obligations

- Equity distributions

Distribution gating tied to coverage ratios prevents structural leakage during stress periods.

Escrow is not administrative convenience. It is downside containment architecture.

III. Covenant Resilience and Coverage Ratios

DSCR and LLCR are not lender formalities. They are institutional shock absorbers.

Coverage ratios must be embedded with:

- Maintenance covenants

- Distribution lock-ups upon breach

- Cure periods tied to reserve injection

- Step-in rights upon persistent default

KPI → Trigger → Remedy logic converts performance deviation into enforceable action rather than discretionary negotiation.

Covenant resilience is credit enhancement.

IV. Governance Enforceability

Institutional allocability requires governance architecture at both AssetCo and HoldCo levels.

Key controls include:

- Independent oversight

- Veto protections over refinancing

- Substitution clauses for underperforming operators

- Defined reporting standards aligned to IC documentation norms

Governance is not oversight theatre. It is capital preservation.

V. Refinancing Visibility from Inception

Platforms structured without refinancing foresight accumulate latent risk.

Refinancing visibility requires:

- Amortisation sculpting aligned to contract duration

- Mid-cycle take-out modelling

- Reserve accumulation for bullet maturities

- Capital stack flexibility

Institutional capital requires exit optionality engineered at entry.

4. Stress-Case Analysis: Testing Cashflow Integrity

Allocability is proven under stress, not base case.

FX Shock:

USD-linked or indexed revenue frameworks combined with FX reserve layering absorb currency volatility. Without this, local currency depreciation erodes coverage ratios.

Revenue Disruption:

Availability-based contracts mitigate volume risk. SLA enforcement ensures performance-linked payment retention.

Payment Delay:

Escrow discipline and reserve accounts isolate short-term liquidity stress.

Refinancing Risk:

Platforms lacking duration alignment face refinancing cliffs. Structurally bankable platforms accumulate refinancing visibility through covenant discipline and reserve buffers.

Stress-case modelling reveals whether the platform is structurally insulated or merely economically optimistic.

5. Institutional Implications: Clearing Sovereign IC Thresholds

For sovereign wealth funds, allocability requires four confirmations:

Cashflow Integrity:

Is revenue enforceable and prioritised through waterfall sequencing?

Governance Enforceability:

Can capital intervene through step-in rights and veto protections?

Duration Alignment:

Does contract tenor exceed debt amortisation schedule with margin?

Exit Visibility:

Is refinancing optionality engineered from inception?

When these conditions are satisfied, infrastructure ceases to be narrative and becomes institutional exposure.

Cashflow hierarchy is the bridge between development activity and capital preservation.

6. Controlled Strategic Close

If infrastructure becomes allocable only when cashflow hierarchy is engineered with covenant resilience and escrow discipline, the next structural question is more demanding:

Can governance control preserve capital across jurisdictions when contractual frameworks are tested under political and liquidity stress — or does allocability ultimately depend on who holds enforceable authority when volatility emerges?