- Home

- Blog Standard

- Insights

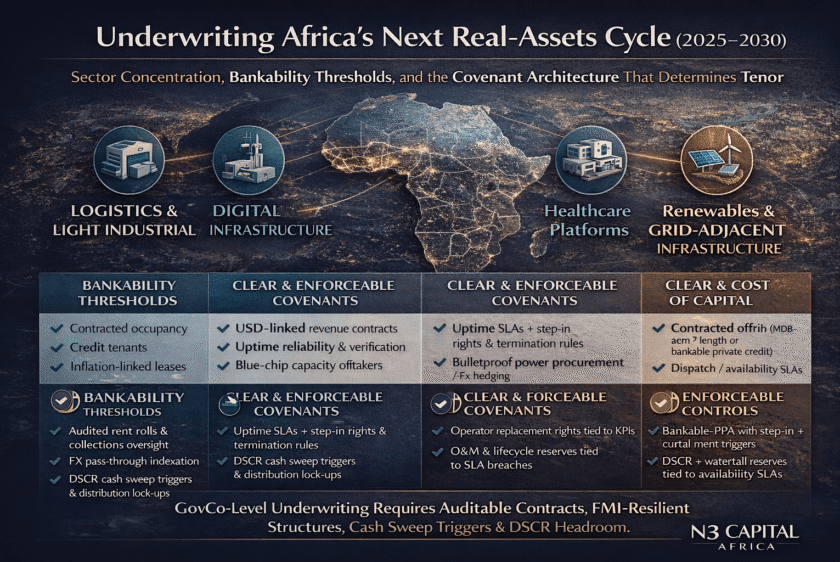

- Underwriting Africa’s Next Real-Assets Cycle (2025–2030): Sector Concentration, Bankability Thresholds, and the Covenant Architecture That Determines Tenor and Cost of Capital

12

Mar 2026

Underwriting Africa’s Next Real-Assets Cycle (2025–2030): Sector Concentration, Bankability Thresholds, and the Covenant Architecture That Determines Tenor and Cost of Capital

By Sir Felix Modebe B.Sc., M.Sc., MBA, FRICS, CCIM, KSJI

Visionary Founder-Leader | N3 CAPITAL AFRICA

Institutional capital is re-shaping African real assets because the underwriting problem has become clearer: FX risk, utilities reliability, and enforcement quality now determine whether long-tenor capital can hold the asset through stress. Demographics and the infrastructure gap create demand, but committees price what they can control—contracted cashflows, measurable performance, and credible remedies when performance fails.

The Institutionalization Wave—What Has Actually Changed

The shift is not “more interest.” It is a higher bar on bankability: tighter documentation, audit-grade reporting, clearer security packages, and governance rights that survive downside. Committees increasingly require standard covenants, reserve waterfalls, and step-in mechanics rather than bespoke exceptions.

Asset buying focuses on acquiring properties; platform underwriting focuses on replicating controls, governance, and reporting across multiple assets to reduce idiosyncratic risk and improve exitability.

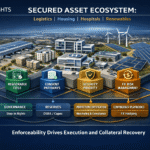

Where Capital Is Concentrating (2025–2030) and Why

Logistics and light industrial

What investors are paying for: contracted occupancy, credit tenants, inflation-linked escalations, and functional assets tied to trade corridors and last-mile distribution.

What can break bankability: title/security weakness, tenant concentration, capex backlog, and FX-driven cost spikes that erode net operating income.

Controls that fix it: enforceable lease covenants, reserve accounts for lifecycle capex, repair-and-maintain obligations, audited rent rolls, and distribution lock-ups linked to covenant breaches.

Digital infrastructure (data centres, fibre-adjacent real estate)

What investors are paying for: contracted, USD-linked or USD-referenced revenues where feasible, uptime-linked performance, and anchor tenant quality. Stabilized assets in some markets have been discussed in the 6.5–8.5% cap rate band, with 9–11% development yields cited for well-structured builds (market-dependent).

What can break bankability: power reliability, EnergyCo under-performance, and concentration risk in tenant mix or supply chain.

Controls that fix it: uptime SLAs with independent verification, cure/termination triggers, step-in rights, O&M and spares reserves, and cash sweeps when performance or financial covenants drift.

Healthcare real assets (hospital and clinic platforms)

What investors are paying for: demand durability with payer discipline, collections mechanics, and continuity of operations (power/water/oxygen/cooling).

What can break bankability: weak payer collections, operator execution, utilities downtime, and ungoverned capex creep.

Controls that fix it: operator KPIs with replacement rights, clinical governance oversight, utilities uptime covenants, lifecycle capex reserves, and reporting triggers tied to AR/denials and service continuity.

Renewables and grid-adjacent infrastructure

What investors are paying for: contracted offtake, predictable dispatch or availability regimes, and clear tariff/indexation logic.

What can break bankability: curtailment, offtaker credit, FX pass-through friction, and E&S non-compliance that blocks financing.

Controls that fix it: bankable PPAs, step-in and termination payment mechanics, DSRA and cash waterfall protections, and enforceable E&S covenants with monitoring and cure rights.

Pan-African Market Lens: “Bankability Signals” by Country

- Nigeria: FX pathway constraints can be binding; title/security varies by state; permitting timelines can be uneven; power reliability often requires embedded solutions; enforcement is improving but remains documentation-sensitive.

- South Africa: FX pathway generally clearer; stronger security and legal enforceability; permitting is process-heavy but legible; grid reliability can be variable; enforcement is comparatively robust.

- Kenya: FX management and convertibility generally workable; land and permitting can be structured with discipline; power reliability is typically stronger in key nodes; enforcement practical when contracts are tight.

- Ghana: FX volatility can surface quickly; security quality depends on documentation and counterparties; permits are improving; utilities can be a constraint; enforcement benefits from conservative structures.

- Tanzania: FX and repatriation require proactive structuring; title/security diligence is central; permits can be manageable with local execution; utility reliability varies; enforcement is workable when governance is clear.

- Namibia: smaller market but improving investability; title/security tends to be clearer; permitting is relatively predictable; power reliability is the key watch item; enforcement practicality is generally supportive.

- Zambia: FX and sovereign sensitivity require buffers; security and permits demand careful diligence; power availability can be uneven; enforcement improves with strong counterparties and conservative covenants.

- Rwanda: governance and permitting are typically more predictable; FX pathways still need planning; title/security can be structured; utilities reliability is improving; enforcement tends to be practical with disciplined documentation.

- Côte d’Ivoire: growing regional hub dynamics; FX pathway benefits from monetary framework but still needs structuring; title and permits require diligence; utilities are improving; enforcement is strongest when contracts are standardised.

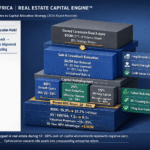

Institutional Underwriting: The Control Stack (IC-Ready)

- Governance & decision rights: reserved matters, capex approvals, operator replaceability, related-party controls, audit and information rights.

- Financial covenants: illustrative DSCR/LLCR floors, cash sweep triggers, distribution lock-ups, covenant cure mechanics.

- Reserve accounts: DSRA (where debt is used), lifecycle capex, O&M/spares/insurance reserves with clear waterfall rules.

- Reporting triggers: monthly KPI pack, quarterly covenant certificate, annual audit, incident escalation protocol (uptime, collections, capex variance).

- FX risk mitigants: ring-fenced accounts, hard-currency payer pathways where feasible, distribution gating tied to convertibility and covenant compliance.

IC Implications: What Boards Should Decide Now

- Tenor will follow enforceability: stronger covenants and remedies support longer duration and tighter pricing.

- Platform replication is the allocator edge: standard controls reduce idiosyncratic risk and improve exitability.

- Utilities resilience must be treated as a credit layer, not an operational detail.

- “Institutional-ready” should mean audited reporting, covenant headroom, and governance rights that operate in downside.

- FX risk must be structured, monitored, and gated—not assumed away. (N3 CAPITAL AFRICA frames this as control-first underwriting for scalable real assets.)

Serious question for allocators: What is your minimum control threshold for scaling Africa exposure—FX mitigants, step-in rights, or reserve-account discipline?