29

Dec 2025

Why Private Credit Is Reshaping African Commercial Real Estate Finance: The New Backbone of CRE Financing

By Sir Felix Modebe B.Sc., M.Sc., MBA, FRICS, CCIM, KSJI

Visionary Founder-Leader | N3 CAPITAL AFRICA

African commercial real estate faces a $200 billion financing gap through 2030. Traditional banks—constrained by Basel III regulatory requirements, post-pandemic conservatism, and currency volatility concerns—no longer meet capital demands of Africa’s explosive infrastructure growth. Private credit emerges as the strategic solution: flexible structures, patient capital, and institutional sophistication enabling transactions impossible under conventional banking frameworks.

The Global Private Credit Surge Meets African Opportunity

Private credit assets under management exploded from $350 billion (2010) to $850 billion (2024), yet Africa represents less than 2% allocation despite offering superior risk-adjusted returns. While mature markets deliver 4-7% yields, African commercial real estate private credit generates 12-18% USD returns backed by demographic momentum, urbanization velocity, and structural supply constraints.

Africa’s Supercycle Drivers: 500 million additional urban residents by 2050 require 2.5 billion sqm commercial infrastructure. AfCFTA implementation drives $80 billion logistics investment. Corporate real estate optimization creates sale-leaseback and build-to-suit demand totaling $150+ billion. Traditional bank capacity: $40-50 billion deployable capital. The gap creates unprecedented private credit opportunity.

Why Traditional Banking Falls Short

Basel III Constraints: Commercial real estate loans carry 75-150% risk weights versus 35-50% for residential mortgages, requiring banks to hold 2-4x more regulatory capital per dollar lent—rendering many institutional-scale transactions economically unviable.

Operational Limitations: Banks provide 40-55% LTV financing versus 65-75% required for competitive development economics. Tenor preferences span 3-7 years versus 10-15 year requirements for African real estate. Local currency lending at 15-25% interest rates destroys project economics while USD exposure creates balance sheet vulnerabilities.

Post-2020 Conservatism: Commercial real estate NPLs increased 35-60% across Nigeria, Kenya, Ghana (2020-2022), driving defensive postures emphasizing capital preservation over growth. Credit committee rejection rates exceed 60-80% for CRE projects regardless of quality.

Currency & Liquidity Challenges: Nigerian Naira depreciated 60% (2020-2024), Kenyan Shilling 25%, Ghanaian Cedi 45%—destroying local currency loan economics. Limited local liquidity ($800 billion total African deposits excluding South Africa), tenor mismatches, and geographic fragmentation prevent efficient capital allocation.

Private Credit’s Structural Advantages

Flexibility: Bespoke structures with interest-only periods during development, cash flow-based amortization, negotiated covenants, and equity participation features. Customization impossible in standardized bank documentation.

Patient Capital: Closed-end fund structures (7-12 year lives) align with African development timelines. Direct lender relationships enable collaborative workout solutions versus rigid bank default cascades.

Institutional Sophistication: Specialized real estate expertise, emerging market risk management frameworks, cross-border structuring capabilities, and capital markets access providing liquidity mechanisms unavailable to traditional bank portfolios.

Speed & Certainty: Capital commitments in 30-60 days versus 90-180 days for banks, providing competitive advantages in time-sensitive transactions.

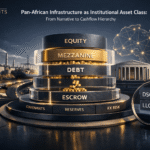

Transaction Structures Enabling Viability

Sale-Leaseback: Private credit purchases corporate real estate ($15-50M per transaction) providing immediate liquidity while structuring long-term leases (15-25 years). Generates 8-12% cap rates with inflation-protected escalations.

Build-to-Suit Financing: Development capital for purpose-built facilities with pre-signed tenant commitments (15-25 year leases) eliminating market absorption risk. Enables 65-75% LTV leverage with 12-16% yields.

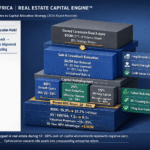

Development & Mezzanine: Construction financing (12-18% rates, 55-70% LTV) and subordinated debt (14-18% IRR) filling gaps traditional banks won’t bridge. Preferred equity structures (15-20% distributions) provide patient capital with downside protection.

Institutional Investor Appetite

African CRE private credit delivers compelling returns: senior debt 10-14% yields, mezzanine 14-18% IRR, preferred equity 15-20% distributions—versus developed market comparables at 4-7%, 9-12%, 10-14% respectively.

Diversification Benefits: Low correlation to public equities (0.15-0.35), negative correlation to bonds, geographic frontier market exposure, and inflation hedging through floating rates and rent escalations linked to local inflation (8-15% annually).

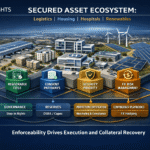

ESG Alignment: Green building certification, solar integration, employment creation, and community development satisfy institutional mandates from sovereign wealth funds, pension funds, and impact investors—reducing cost of capital while demonstrating measurable social value.

N3 Capital Africa’s Strategic Framework

Our platform positions private credit as African CRE financing backbone through:

- Geographic Expertise: Operational presence across Nigeria, Kenya, South Africa, Ghana

- Capital Network: Strategic relationships with DFIs (IFC, AfDB, DFC), sovereign funds, family offices

- Transaction Sophistication: Optimal capital stack engineering, USD structuring, political risk mitigation

- Active Management: Quarterly inspections, monthly reporting, continuous performance optimization

Market Projections: $15-25 billion cumulative private credit deployment 2026-2030, 35-45% annual growth, 15-20 Africa-dedicated funds launching, 3-8% institutional allocation (versus <1% currently).

Strategic Conclusion

Private credit transforms African commercial real estate by providing capital structures, investment horizons, and institutional sophistication unavailable from regulatory-constrained banks facing currency challenges and post-pandemic conservatism.

For developers and corporate strategists, private credit enables project execution and balance sheet optimization impossible under conventional frameworks. For institutional investors, African CRE private credit delivers 12-18% USD yields with portfolio diversification, inflation protection, and ESG alignment.

The strategic question is no longer whether private credit becomes mainstream African CRE financing, but how rapidly stakeholders establish partnerships with sophisticated capital providers before competition intensifies and return premiums compress.

N3 Capital Africa | Pan-African Commercial Real Estate Capital Platform

Private Credit Solutions | Build-to-Suit Development | Sale-Leaseback Transactions

www.n3capitalafrica.com | info@n3capitalafrica.com